If there’s one thing that strikes fear into the hearts of Bay Area homeowners, it is getting a low appraisal when selling their home. That is perfectly understandable, of course: Bay Area home prices are so high, how could anyone really justify them? Yet every year, tens of thousands of homes are sold in the Bay Area, almost all of which had an appraisal performed in the process…and they still closed, just fine. In this article, I’ll explain why low appraisals don’t determine home value in the Bay Area, so you can relax and focus on other important aspects of the sale.

I myself have personally sold well over 400 homes by now – and have been in quite a few more transactions that didn’t close but which did have an appraisal performed – and from where I sit (at the heart of many more Bay Area home sales than most people will ever come close to), I have difficulty thinking of more than a small handful of instances where the sale of a home in the Bay Area I was involved in got a low appraisal…and not a single instance of when it actually caused the sale to fall apart.

Understanding Bay Area Home Appraisals

A home appraisal is a critical step in the home selling process. This process involves a detailed inspection of the property’s interior and exterior, coupled with an analysis of recent comparable sales and market trends in the neighborhood.

The appraisal report, which includes the appraiser’s opinion of value, guides lenders in determining how much they’re willing to lend potential buyers. Thus, a low appraisal value can complicate the financing process, potentially stalling or even derailing your home sale.

If there’s anything a buyer and seller need to know about the appraisal process, it is that the the value the appraiser gives is just an opinion. It is not a fact. This is the reason why a seller is not required to give a buyer copies of any appraisal reports the seller may have. On the other hand, the seller is required to give buyers any copies of inspection reports, governmental records, and disclose any other material facts they are aware of regarding the property. The existence of the appraisal itself is a fact, but it is immaterial, because the value given in the appraisal is simply an opinion (albeit allegedly an “expert” opinion).

For the purposes of a mortgage loan, residential appraisals are performed using the Uniform Standards of Professional Appraisal Practice (USPAP) guidelines. Most appraisals are completed using the Fannie Mae URAR (Uniform Residential Appraisal Report) Form 1004. These URAR appraisals require that the appraiser give a certification for the appraisal report. This certification contains standard language, for example:

I developed my opinion of the market value of the real property that is the subject of this report based on the sales comparison approach to value. I have adequate comparable market data to develop a reliable sales comparison approach for this appraisal assignment. I further certify that I considered the cost and income approaches to value but did not develop them, unless otherwise indicated in this report. (emphasis added)

Everyone wants to know…

Purpose of an Appraisal

Another common misunderstanding is that the purpose of an appraisal is to determine how much a home is worth. That is true in a manner of speaking, and the URAR form 1004 does say:

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property. (emphasis added)

The words “adequately supported” are very important to understanding the practical purpose of the appraisal.

Many buyers and sellers are unaware of this, but the appraiser is given a copy of the purchase contract before they perform their appraisal report. This means that the appraiser knows the contract sale price. In practice, the appraiser is looking to support the contract sale price.

If the appraiser was not privy to the contract sale price, I guarantee you that absent that guidance, appraisals would in many cases be far higher, or lower, than the contract price. Now imagine if the appraiser didn’t even have access to the MLS, and could not see the list price for the property…how far off from the contract sale price might the appraiser be then?

Understanding that the practical purpose of the appraisal is to support the sale price, it would be no surprise to learn that in almost all cases, the appraised price is either:

- Exactly the contract sale price

- $1,000 or $10,000 more than the contract sale price

- Some other number within 1-2% over the contract sale price

Of course, sometimes, the appraisal price is less than the contract price. This can happen when an appraiser has very little understanding of the market, or, in some cases, there simply is no way for the appraiser to support the sale price, try as s/he might. I’ll discuss low appraisals a bit further down, and why in most cases, there is little to worry about there. But before I get to that, I’d like to discuss a bit about how appraisers come up with the values in their reports.

Appraisal Methods

In real estate appraisal, three primary methods are used to estimate a property’s value:

- The sales comparison approach

- The cost approach

- The income approach

The cost approach, often used for new construction, estimates the cost to replace or reproduce the property, minus depreciation.

The income approach, more applicable to investment or commercial properties, calculates value based on the income the property generates, considering factors like rental income and operating expenses.

Lastly, the sales comparison approach, most commonly used for residential resales, involves comparing the property in question to similar properties that have recently sold in the area, adjusting for differences like size, condition, and location. This method is favored for residential properties because it directly reflects the current market trends and what buyers are willing to pay for similar homes.

While a URAR appraisal will include opinions of value using all three methods, it will indicate which method was most strongly considered, and for residential properties, that method is, (almost) invariably, the sales comparison approach.

Because the sales comparison approach is the valuation method that is relied on, it is rare for any home to appraise at a low price in the Bay Area. That’s because the way the sales comparison approach works is to make “adjustments” to the comparable properties to compensate for the ways they differ from the subject property. And it is with these “adjustments” that the appraiser is (almost always) able to support the contract sale price.

Adjustments to the Comparables to Establish the Subject Property’s Value

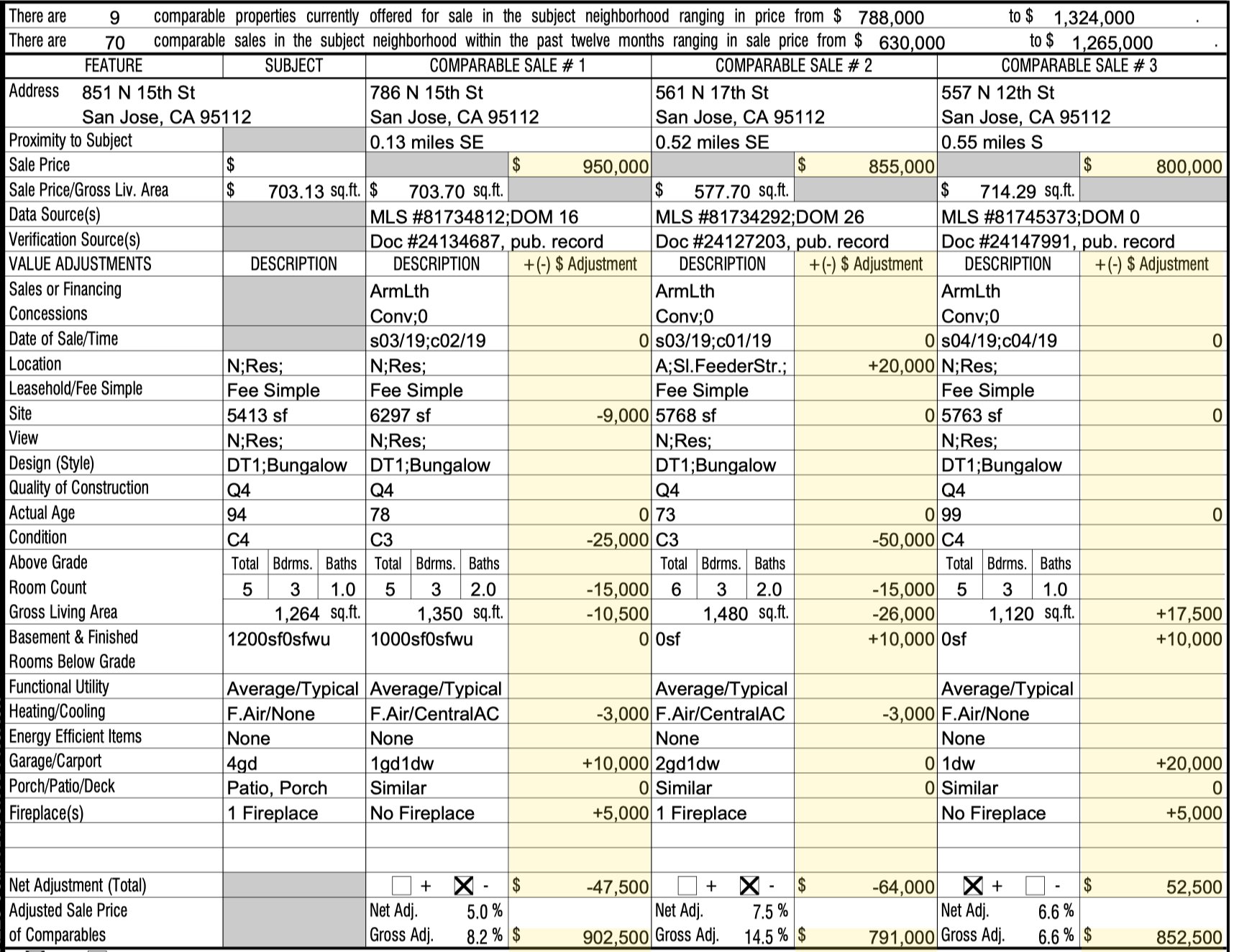

A the heart of the URAR appraisal form is the Residential Sales Comparison Grid. An example of the sales comparison grid from an appraisal of a home in San Jose is below:

Appraisal Adjustments URAR Form 1004

As you can see, there are three comparable sales in the grid, and they are compared to the “subject” property (the property being sold). In this example, adjustments have been made for lot size, condition, room count, gross living area, heating/cooling, garage/carport, and the fireplace. In the grid above you can see that at the top, each comparable sale has the sale price, and at the bottom, each as the “adjusted sale price of comparable.”

To adequately support the appraiser’s opinion of value, the appraiser’s value opinion will need to be within the range of the adjusted sale prices. In this example, the appraised value would need to be between $791,000 (the lowest adjusted value) and $902,5000 (the highest adjusted value). In this particular case, the appraiser determined the home was worth $860,000 (or very close to the mid-point between the high and low sale prices … nice!).

In the appraisal report remarks, the appraiser would indicate which comparable(s) received the most emphasis in determining the subject’s value. Typically, these are the comparables which required the least adjustment.

How Appraisal Adjustments are Determined

So now you may be wondering, where do these adjustment values come from?

I used to wonder that myself. In fact, years ago, I enrolled in a college-level appraisal course specifically to discover how appraisers came up with these adjustment values. It turns out though that there is no standard set of adjustments used by the appraisal industry. Like the appraisal value itself, the adjustments which are made are also just the opinion of the appraiser.

The adjustments are supposed to be supported by market data, although nowhere is it explained how exactly market data specifically informs those adjustments. There are some appraisal techniques you can point to like paired-sales analysis to attempt to quantify how much any adjustment should be for a particular feature in any given market, but this isn’t actually part of the URAR appraisal report.

Now we can clearly see the reasons why appraisals so rarely come in low in the Bay Area:

- The appraiser knows the contract price, and their job is to show that the comparable sales support that contract price.

- The appraiser picks the comparables which they feel will best support that price, and massage the adjustments so that they reasonably prove to the loan’s underwriter that the contract price does not exceed fair market value.

For Best Results

What Happens When a Home Appraisal Comes in Low?

Rare though it may be, it is certainly possible that an appraisal will come in below the contract sale price. While I have seen this happen a handful of times, I can’t think of when I have personally seen it cause a deal to fall apart. While I have heard of low appraisals blowing up sales, I usually hear about this happening in other states or areas far removed from the Bay Area.

Regardless of where or when a low appraisal comes in, there are several possible outcomes:

Renegotiate the Purchase Price

The buyer and seller could renegotiate a new sale price that aligns with the appraisal value. While this may reduce the seller’s profit, it could keep the home sale on track. The seller may agree to lower the sale price to the appraised value, or may lower it somewhat with the buyer making up for the difference.

Buyer increases the Down Payment

The buyer could consider increasing their down payment to cover the gap between the appraised value and the contract price. However, this approach might not be feasible for all buyers, although in the Bay Area, many buyers do have the financial capacity to at least marginally increase their down payment if need be.

In the Bay Area, it is common to see buyers with large down payments far in excess of the minimum required by the loan’s debt-to-equity ratio. If a buyer is putting 30%, 40%, or 50% down, the chance of a low appraisal blowing the loan’s debt-to-equity ratio is close to nil. With a down payment this large, most buyers will not even ask for an appraisal contingency, or it is easy to remove it via negotiation if they do.

The deal falls apart

Depending on the terms of the contract, the buyer may choose to walk away from the deal if the appraisal comes in low, particularly if that the buyer has an appraisal contingency, which I will discuss below.

The Role of the Appraisal Contingency

One of the terms of many purchase contracts is an appraisal contingency. The appraisal contingency gives the buyer a certain number of days to get an appraisal, and if the buyer cannot have an appraisal performed in that time (after having made a good faith effort to do so) or if the appraisal comes in below the target price, the buyer may cancel the contract and have their earnest money deposit returned to them.

Appraisal Contingency

In the past few years, the California Association of REALTORS has modified their purchase contract so that the buyer may specify that there is a minimum appraised value which may be less than the contract sale price. This difference between the sale price and appraised price is known as an “appraisal gap,” and while the standard purchase contract does now allow for a maximum contractual appraisal gap, I don’t see a lot of offers written with an allowance for it. I think the reason for this is because REALTORs know that low appraisals are rare, and in the competitive Bay Area real estate market, having an appraisal gap written into the contract makes the buyer look weak.

Earlier, I did mention that while I have seen a handful of low appraisals, I can’t think of a single instance of when that scuppered a deal. That’s because the lenders do not actually require that the property be sold at the appraised price (or below it).

Making up for an Appraisal Shortfall

What lenders really care about is that the loan has the debt-to-equity ratio required by the loan guidelines. For the sake of simplicity, let’s say that a buyer went into contract on a home with a $1,000,000 sale price. As required by the buyer’s loan guidelines, the buyer was putting down 20% of the purchase price, or $200,000. 80% of the purchase price would therefore be paid for with the loan (debt), and 20% of the price would be paid in cash (and becomes the buyer’s equity in the property).

Let’s say though that the property only appraises for $950,000. Does this mean the deal is off?

If the buyer had an appraisal contingency based on the $1,000,000 price, the buyer could choose to cancel the sale and walk away. However, the lender would be perfectly fine to loan on the property…but they would want to loan less.

If the appraisal were to come in at $950,000 then the lender would only loan $760,000 on the property ($760K is 80% of the $950,000 appraised value, the maximum amount allowed by the loan guidelines in this example). The buyer would then need to increase their down payment from $200,000 to $240,000 ($1,000,000 sale price minus the maximum $760,000 loan amount = $240,000) to maintain the 80/20 debt-to-equity ratio and still maintain the $1,000,000 sale price.

Many buyers in the Bay Area do indeed have sufficient cash so that they can make up for appraisal shortfalls – unless the shortfall is dramatic, in which case, even if they are able to make up for the difference, may lead the buyer to second-guess the true value of the property and walk away regardless.

Conclusion

While a low appraisal can be stressful for both the buyer and the seller, it doesn’t have to derail the home sale…and in fact, in the Bay Area, it rarely happens and even less frequently does it cause a sale to fall apart. By understanding the appraisal process and being prepared to negotiate, you can navigate this situation successfully. Whether you’re a buyer or a seller, working with a knowledgeable real estate agent can provide valuable guidance and support. Remember, low appraisals are just part of the real estate landscape, and with the right approach, you can still achieve a successful home sale.

The Secret Sauce for Selling